Who Owns the Automated Future?

The Fourth Dialogues with David Shapiro · Part I

Below is a transcript of a conversation I had with the Fourth Founding Project, which is techno-progressive group interested in the future of politics, humanity, technology, and government in the United States. They reached out to me due to my work on Post-Labor Economics and my upcoming work on Structural Realism. The transcript has been cleaned up from our recording.

Fourth Founding Project: If you had to explain post-labor economics to someone encountering the phrase for the first time, where would you start?

David Shapiro: I would start with the premise, which is that automation has been advancing for decades.

Manufacturing in America peaked as a share of nonfarm employment in the early 1950s, when it accounted for about a third of nonfarm jobs. Manufacturing then kept declining as a share of employment. Later, in 1979, manufacturing peaked in absolute employment, at roughly 19.6 million workers. After that, the absolute number of manufacturing workers began falling too.

So there are two different things happening. First, a sector can become less central to the economy. Then the number of workers in that sector can fall in absolute terms.

When people like me say that AI and robotics are going to affect service-sector jobs, white-collar jobs, and knowledge work, we are describing a continuation of something that has already happened. The same thing that happened to farm labor, and the same thing that happened to manufacturing labor, is now coming for knowledge work. That is the premise behind post-labor economics.

Then people say, “Well, technology always creates new jobs.” I think that misses the deeper point. Technology creates new supply and new demand. It just so happens that humans have historically sat in that loop between supply and demand. Markets need goods and services. They need supply and demand to clear. There is no law of economics saying a market must have human labor forever. Human participation was necessary for most of history. That does not make it a permanent law of economics.

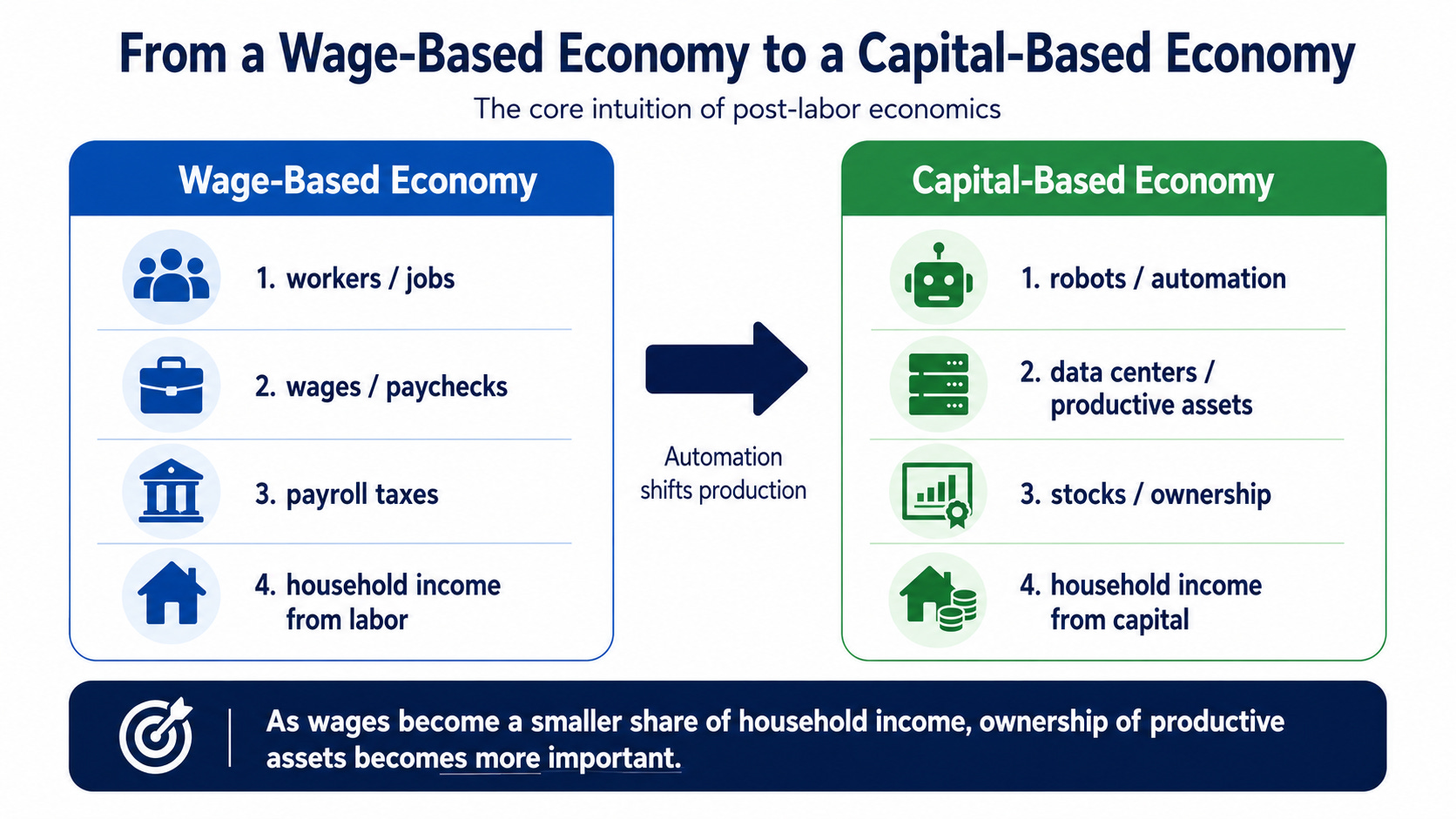

Once you accept that premise, the question becomes: if wage labor has been the primary distribution mechanism in a labor-based system, what happens when labor is no longer the main mechanism?

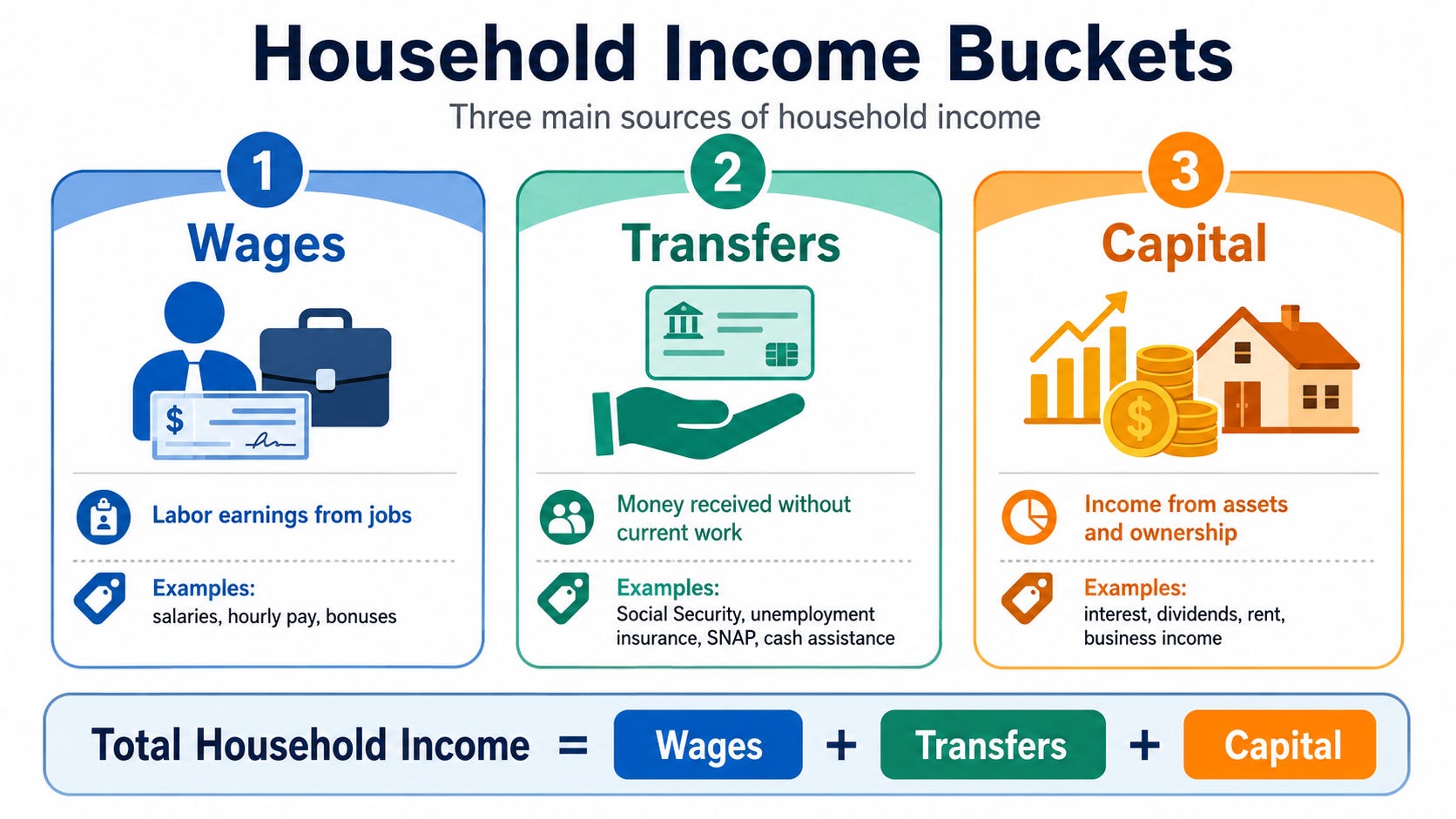

That is why I call it post-labor economics. The core macroeconomic concern is household income and aggregate demand. Aggregate demand is the amount of money households have available to spend. So the problem you are trying to solve is simple: how do we get money into households?

Household income has three buckets. The first is wages. That is by far the largest bucket for most households. The second is transfers: welfare, UBI, Social Security, veterans benefits, SNAP, public transportation, public education, and other forms of tax-and-spend or in-kind value. The third bucket is capital. That is ownership stakes: rental properties, stocks, bonds, and other assets that produce returns.

At the top of the income distribution, capital already plays a much larger role. The exact numbers vary depending on where you draw the line, but the basic point is that capital income is already a real household income mechanism. It is just highly concentrated.

If wages decline, then what are we left with? We have transfers and we have capital. Transfer dependence is dangerous, because the government can turn the tap off. So by process of elimination, we have to move toward a much broader capital-centric distribution mechanism.

That may sound strange at first. But if most of the economy has been running on wages, why couldn’t a future economy run much more heavily on capital distributions? That is post-labor economics in the elevator pitch.

So the issue is not only whether specific jobs disappear. The deeper question is whether wage labor continues to function as the main way income reaches households.

David: Exactly. People often want to debate job loss as if the issue is whether this job or that job survives. That matters, of course, especially for the person in that job. But at the macro level, the problem is household income.

If wages are the main channel, and wages weaken, then what replaces them? Transfers can replace some of them. Capital can replace some of them. But those are very different systems. They have different political implications. They create different forms of power.

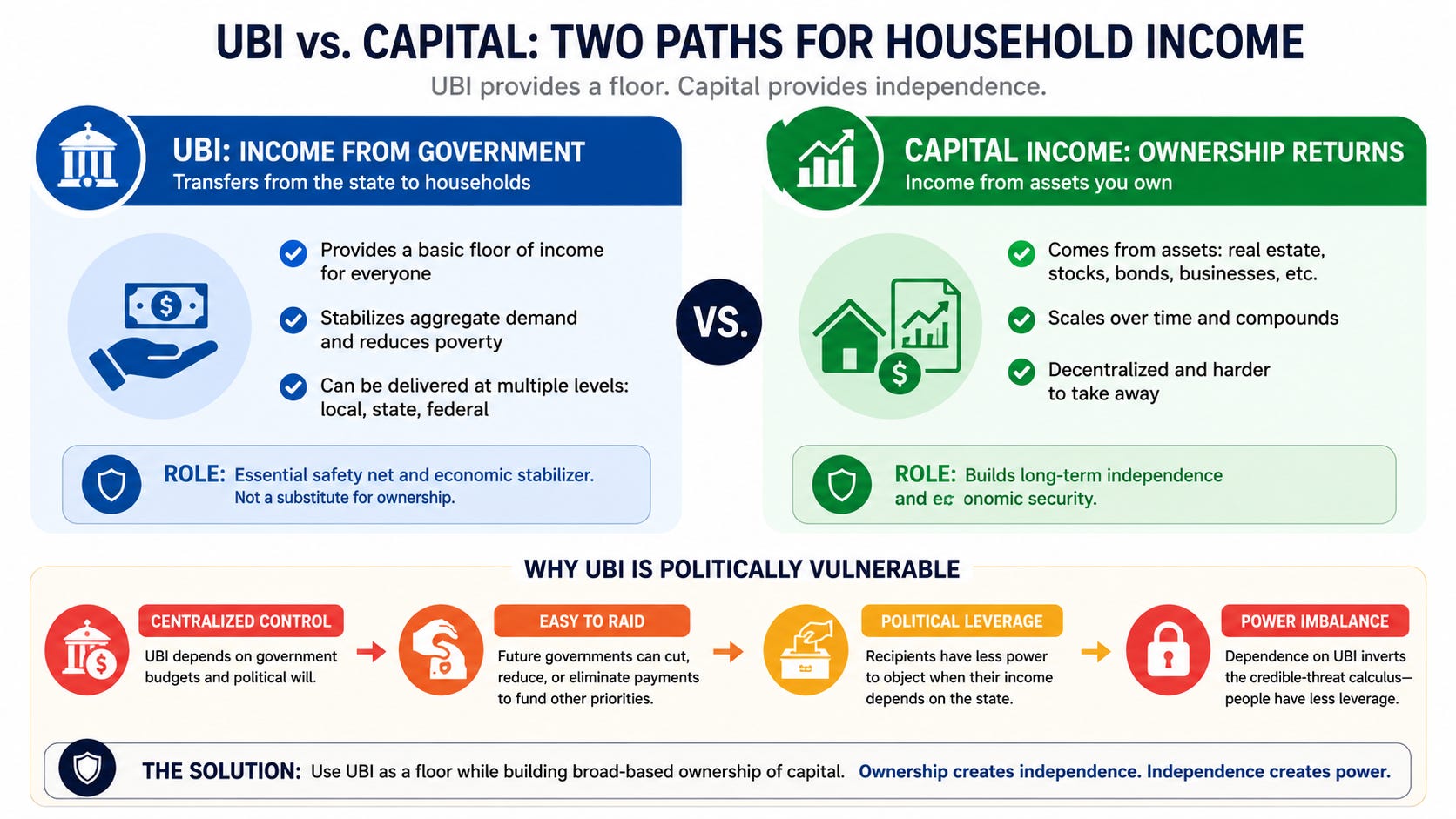

A lot of people hear this and immediately think of UBI. Does UBI give people the bridge they need into a post-labor economy, or does it create a new vulnerability if people lack control over it?

David: UBI is probably more than a bridge. I think some form of UBI is likely necessary as a permanent feature. The reason is that it takes time to accumulate capital.

Think about your ideal personal financial situation. You might own your house. You might own rental property. You might have an annuity, dividends, Treasury bills, bonds, and conventional stocks. You own a bunch of different assets. That is what I envision for the future, except every household has some version of that at multiple levels.

You could have UBI from your city or county. You could have it from your state. You could have it from the federal government. I think we should probably have all three.

But UBI should not be the lion’s share of your income. I would never advocate against UBI. I am arguing against putting all of your eggs in that basket.

From a macroeconomic perspective, UBI takes money from concentrated areas, such as government, corporations, or wealthy people, and puts it into households so aggregate demand stays higher. That is the core function of UBI. It gets money into households.

But from a power perspective, UBI has a weakness. It can invert the credible-threat calculus.

Right now, workers still have forms of leverage. They can quit. They can refuse labor. They can strike. They can shut something down. If your income comes primarily from a government transfer, the government can become the one with the threat. It can turn the tap off.

That is why ownership matters.

So UBI helps solve the income problem, but ownership helps solve the power problem.

David: Right. Ownership is stronger because ownership is legal and physical control over a resource.

If you own a data center, you have control over the power switch. If you own the port, you can shut the port down. If you own shares in the companies that produce the wealth of the automated economy, you have a claim on the returns. If those are voting shares, households do not only receive returns; they have a voice, potentially a controlling voice, in how those companies operate.

That is why I think decentralized, distributed ownership is so important. I want to be clear that I am not arguing for the state to concentrate ownership. I am arguing for the opposite: distribute ownership stakes as broadly as possible to as many people as possible.

If every household has voting shares and stakes in robotics companies, data centers, the power grid, chip manufacturers, and other core assets, then households benefit from what those companies do. They also have a say in how those companies operate.

That expands democracy into the marketplace.

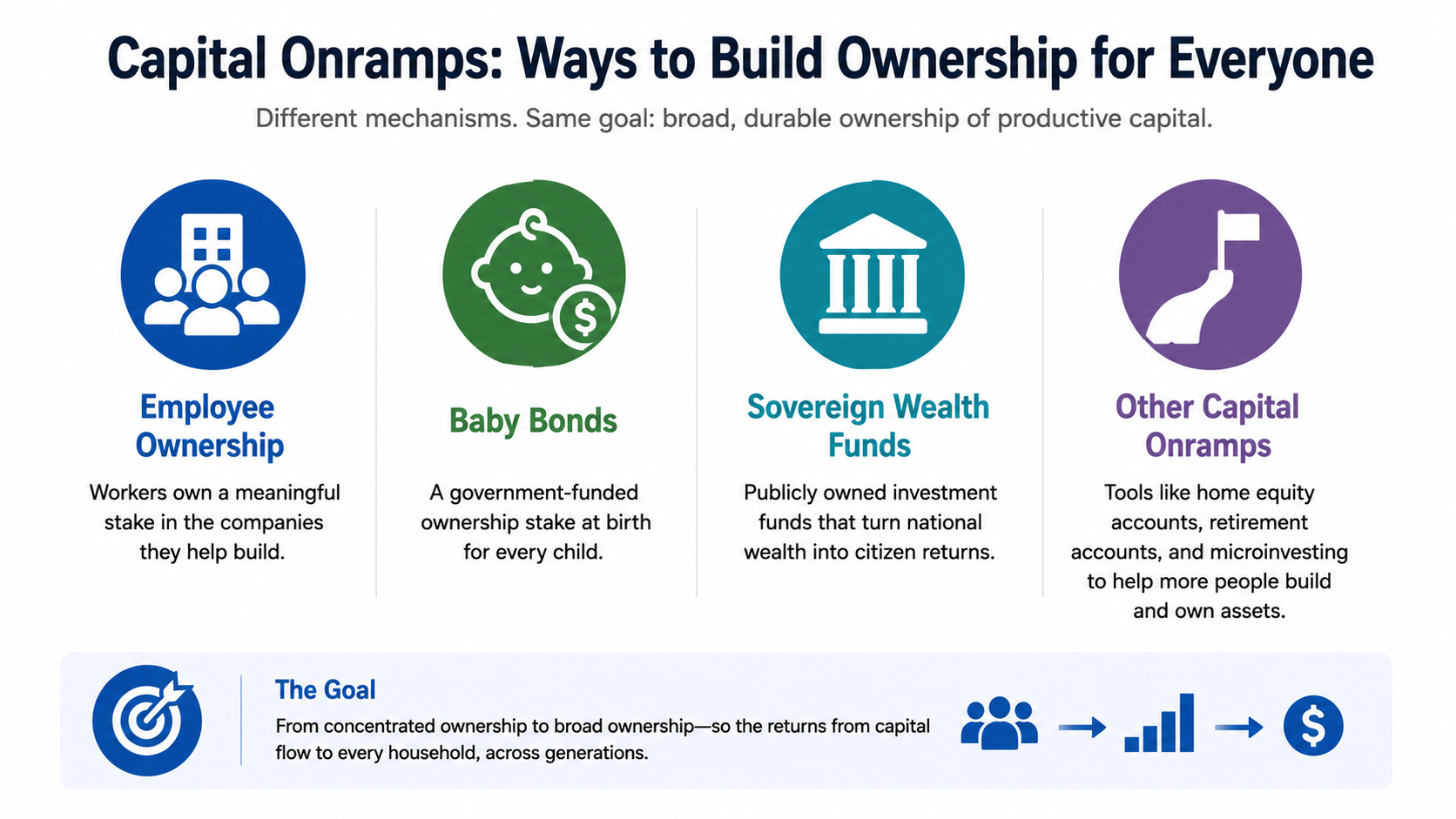

When you say ownership, what are the actual mechanisms? How does ownership move from being concentrated in private hands to being broadly held by households or public institutions?

David: Public ownership is one vector. You could have a sovereign wealth fund at the national level. You could also have state wealth funds. One way to capitalize those funds would be to let companies pay some portion of their taxes in shares.

Instead of a one-time tax payment, the public gets an ownership stake. You would cap the stake so you do not distort the market or create a de facto takeover. Maybe that cap is five to ten percent. You could imagine a policy where a company contributes one percent of its shares each year for ten years, in lieu of some tax obligation. At the end of that period, the public wealth fund owns a meaningful stake and receives the associated returns.

There are design questions around voting shares. In many sovereign wealth funds, the fund does not get voting shares. That is a debate. I would personally argue that if we move away from labor and wages, the state should have some voting shares, because the state can then vote on behalf of the people. That is a larger conversation, but it matters.

Then there is the question of how the proceeds reach households. One option is in-kind services. The wealth fund helps pay for government services, so the burden on wages and paychecks declines. Another option is direct dividends, where the fund pays households. Both models exist in different forms around the world.

A second vector is making capital accumulation automatic. Employers already do this with matching contributions. For every dollar you invest, they match it. The government could do that too. Some governments have programs that match savings or investments, sometimes at very generous rates.

The deeper principle is default accumulation. If saving and investing are the default choice, people are less likely to opt out. Instead of receiving a dividend check and spending it right away, the default might be that it goes into a baby bond account, a sovereign wealth fund account, or another automatic investment account. People can still make choices, but the system is designed to help households build capital.

There are dozens, probably hundreds, of mechanisms and downstream programs that can make capital accumulation automatic, easy, frictionless, incentivized, and protected. The protected part matters a lot.

Baby bonds are one example. In the U.S. policy debate, the idea is associated with economists such as Darrick Hamilton and William Darity. Piketty has proposed a related universal capital endowment. The shared principle is to give young people a meaningful capital stake as they enter adulthood.

So the goal is less a single program and more an architecture: public funds, household accounts, default investment, and legal protection.

David: Yes. I do not think any one mechanism is enough. UBI alone will not solve it. A sovereign wealth fund, baby bonds, employee ownership…none of them solve it on their own.

You want a portfolio of mechanisms. Some at the national level, the state level, or the city or county level. Some inside firms. Some attached to public resources, or private enterprise. The goal is to create many pathways for households to build and receive capital income.

What about ownership inside firms themselves? Are employee ownership models part of your post-labor framework?

David: Absolutely. I would create more on-ramps for employee ownership.

One of the strongest models is the employee ownership trust. Britain has done important work here. The basic idea is that when an owner retires, instead of selling the company to private equity or shutting it down, there is a legal pathway for the company to transition into employee ownership. The owner gets a tax advantage. The employees get the company.

That is one of the most powerful things we can do to distribute ownership widely. Employee-owned cooperatives and employee-owned companies have been around for a long time. The UK employee ownership trust model has shown that this can work at scale.

In the United States, I would also look for ways to make it easier for C corporations to transition into ESOPs or other employee ownership structures.

This becomes especially important in an automating economy. Imagine you work at a company and the company says, “We are going to automate your job.” That is usually terrifying. But now imagine that everyone who works there has a stock payment plan. You can take a portion of your compensation in stock.

In that scenario, you may be helping automate away your own job, but you are also an owner of the company that becomes more productive. That changes the incentive structure.

Instead of automation only meaning displacement, it can mean ownership.

I would make that a national mission. Create a legal and policy framework that allows companies to automate faster while workers become owners of the gains. That is how we reduce resistance and make the transition less destructive.

Let’s make this concrete. If you were governor of California, with so much of the AI industry in your state, what would you do first?

David: If I were governor of California and had a strong coalition, I would create a state-level wealth fund and capitalize it every way I could.

I would look at the major technology companies and say: instead of simply trying to tax you until you leave, we are going to align incentives. You can receive tax advantages by contributing shares into the public wealth fund. Maybe it is one percent per year up to ten percent. The details matter, but that is the basic idea.

California often creates incentives for wealthy people and companies to leave. I would try to do the opposite. Make it more attractive for them to stay by linking their success to the state’s success. If the companies stay in California, they keep the tax advantages. If they leave, they lose them, but the public keeps the shares already contributed.

Technology companies understand platform lock-in. This would be state lock-in. The state builds a durable public stake in the wealth created by Silicon Valley.

If the proceeds from that wealth fund help pay for public services, infrastructure, or direct household benefits, then Californians have a reason to support the success of those companies. The companies have a reason to stay. The state has a reason to help them grow. That is incentive alignment.

My mental model is that there are four major stakeholders: capital, citizens, the state, and banks. Capital includes the elites and the businesses, because the elites own so much of the businesses. A sovereign wealth fund can align those stakeholders.

In that setup, automation stops being something only capital wants. Citizens, the state, and capital all have a stake in productivity gains, because the gains flow into the fund.

Outside California, a lot of states are dealing with data centers right now. What should state legislatures be doing in relation to data centers and the post-labor economy?

David: A lot of states are already using the leverage they have. Data center moratoriums are an example. When local or state officials slow down or block a project, that is a credible threat against the industry. It says, “We will stop this until you come to the table.”

We can come back to the credible-threat side of this, but the immediate policy point is that data centers create bargaining opportunities.

The key point is that corporations exist because the law allows them to exist. The infrastructure they benefit from, the courts they use, the roads, the energy systems, the welfare state that stabilizes the society around them, all of that comes from public authority. Companies often talk as if government should simply get out of the way. But historically, corporations have always depended on public permission and public infrastructure.

So the question is: what concessions should the public demand?

For data centers, one answer is taxation. You are going to pay more taxes on that data center. You are going to pay for the energy infrastructure. You are going to pay for the water, the land-use impacts, the local burden, and the public systems that make the project possible.

States are already doing some of this because they have direct leverage over siting and permitting. The problem is that they do not yet have a comprehensive post-labor plan. They are using the tools available to them, but the framework is still missing.

At the national level, if there were a governing coalition with the ability to do something big, what would be the first priority? What is the “Medicare for All” version of the post-labor economics agenda?

David: Some pieces are already being discussed or attempted. The Trump administration directed Treasury and Commerce to develop a plan for a U.S. sovereign wealth fund, and it has created Trump Accounts, a baby-bond-like program with a one-time $1,000 federal contribution for eligible children born from 2025 through 2028. I do not think either is enough unless the institutions are designed and protected properly.

The real priority is a constitutionally-protected sovereign wealth fund.

There are lots of ways to capitalize it. Some people want separate funds for mineral rights, carbon capture, spectrum, data centers, or other assets. Maybe there are legal or managerial reasons to separate them. But conceptually, I would rather see one national public wealth fund capitalized from many sources.

The key is protection. If it is only a normal statute, then a future administration can raid it, redirect it, or weaken it. A public wealth fund has to be protected from short-term politics. That is why constitutional protection matters.

The next priority is baby bonds or some kind of universal capital account. Then I would build out employee ownership trusts, ESOP transitions, and other on-ramps into ownership.

Those are the main pieces: a protected public wealth fund, universal capital accounts, and easier pathways for employee ownership.

If wage labor declines, public finance also changes. Today, a lot of public revenue depends on wages and income. In a post-labor economy, where does the revenue come from?

David: The government’s funding model has to structurally change.

Today, individual income taxes and payroll taxes provide roughly four-fifths or more of federal revenue. If payroll and income taxes decline because wage labor declines, then you have to ask where the new wealth comes from. It comes from data centers. It comes from robots. It comes from energy production. It comes from chip manufacturing. It comes from the automation technologies.

That is where the taxes have to come from.

When the source of wealth changes, the tax base has to change too. In the future, capital becomes the primary producer. So if you are funding UBI, capitalizing a wealth fund, or paying for public services, the revenue has to come from the productive assets of the automated economy.

Land value taxes are useful as an analogy. Henry George was writing in a world where land was the central asset. The deeper principle is to tax the scarce, valuable, location-specific asset that generates economic rent. In the future, that may mean power plants, the power grid, data centers, robots, foundries, and other infrastructure.

A data center is a good example because you cannot simply move it once it is built. You can choose where to put it, and states will compete for that. But once it exists, it depends on local and national infrastructure. So it makes sense to tax the asset and the resources it consumes.

We already tax resource consumption in many areas. Gas taxes are one example. Sales taxes are another. The basic idea is straightforward: tax the assets and resource flows that generate the new wealth, then use that revenue to fund public services, household income, and public wealth funds.

Are there public assets or commons that should be used to build these funds?

David: I think so. Monetizing the commons is another important pathway.

A lot of commons monetization happens locally. Land value, forests, local resources, local infrastructure. At the federal level, there are different assets, such as spectrum. Spectrum auctions often just flow into the general budget. I would create a rule that some meaningful share of revenue from federal resources or commons has to go into the sovereign wealth fund.

If the federal government owns, controls, or monetizes a public resource, a share of that rent should build public wealth. Alaska does this with mineral revenues through the Permanent Fund. New Mexico has used permanent-fund structures to support education and early childhood programs. The basic model works: take a public resource, capture some of the rent, and convert it into durable public wealth.

That becomes especially important in a post-labor economy, because you need many sources of capitalization. You do not want the whole fund dependent on one industry or one asset class. You want multiple streams.

One concern with sovereign wealth funds is that if they rely too much on one industry, the public interest can become tied to that industry’s survival. If the fund is built on oil, for example, the public may become less willing to move away from oil. Does diversifying the revenue sources solve that problem?

David: Diversification helps. If your sovereign wealth fund is capitalized entirely by oil, you are going to be less eager to shut off the flow of oil. That is a real concern.

But in my research, the bigger risk is governance. The biggest problem is usually that the fund is not well-protected. There are places that had resources, made a lot of money, failed to protect the fund, and ended up broke anyway.

So yes, diversify the revenue sources. Use spectrum, energy, data centers, land value, carbon capture, royalties, and other public rents where appropriate. But above all, protect the fund.

There are established best practices for sovereign wealth funds and public wealth funds. The Santiago Principles are one example. You need rules around governance, withdrawals, transparency, investment policy, and political interference.

What happens if the fund takes a hit? If the stock market declines, or the underlying assets fall in value, do households bear that loss?

David: Any public wealth fund has to deal with the fact that asset prices go down. That is why governance and payout rules matter.

One advantage of a dividend-style payout is that it can vary. Some years the payout is higher. Some years it is lower. If there is no surplus, there may be no payout that year.

That is different from entitlement spending, where people are promised a fixed amount regardless of the government’s ability to pay. A public wealth fund can say: here is the surplus this year, and we are distributing it equally to households.

If the fund owns positive-value assets, households do not owe money when the market goes down. They just may receive a smaller payout, or no payout, in a bad year. And if the fund is structured to receive dividends, then capital gains are not the only source of returns. You may still have income even when asset prices are down.

So there are ways to design around volatility. But again, it all comes back to governance.

So the issue is not simply creating the fund. It is protecting the fund from politics, market swings, and short-term raids.

David: Right. If you create a large public wealth fund, some future governor, legislature, president, or Congress will look at it and say, “That is a lot of money. I can spend that and make myself look good.” If the fund is legally vulnerable, eventually someone will raid it.

That is why I think these funds need constitutional or very strong legal protection. Alaska constitutionally protects the principal of the Permanent Fund. You would want something similar at the national level. Once the fund exists, the principal should be locked away from ordinary politics.

The same logic applies to UBI or any other redistribution policy. If it is simply a program, a future administration can cut it. If it is constitutionally protected, then it becomes a durable part of the social contract.

The post-labor economy needs that kind of durability. You need institutions that make capital accumulation automatic, that distribute returns broadly, and that survive political cycles.

That is the goal: build public and household wealth, distribute the gains of automation, and protect the system so it cannot be captured or raided later.

I'd like to see some capital owned by non-governmental, ideally international, organizations on behalf of everyone and paying dividends to everyone. This could provide a layer of insulation from governments. E.g. ownership of the seas, the atmosphere, Earth orbits, etc. Dual-goals of income to everyone, and protecting their capital (clean water, clean air, flourishing sea life, avoiding a Kessler syndrome, etc.) A foundation to own the moon, another for Mars!

Awesome! Looking forward to your book